From European Payment Systems to High-Frequency Trading: Mastering the Mathematical Foundations and Python Implementations for Production-Ready Machine Learning Pipelines

In the high-stakes world of financial systems and AI, the common adage suggests that “data is the new oil.” From a seasoned practitioner’s lens, this is a bit of a misnomer. Raw data is more like crude ore: high in potential, but fundamentally unusable until it is processed, refined, and engineered into a signal suitable for algorithmic ingestion.

For a machine learning engineer or data scientist, distinguishing between data types isn’t a classroom exercise; it is a high-stakes architectural decision. If you misidentify a feature’s type, your model’s geometry fails. If you ignore the distribution of your numerical signals, your gradients explode. If you treat a temporal sequence as independent observations, your backtesting will lie to you.

As a professional, you will encounter these types in diverse, high-pressure environments:

- European Payment Gateways: Where you must analyze the “burstiness” of SEPA transaction counts (Discrete) alongside the fluctuating processing latency (Continuous).

- Invoice Finance & Factoring: Where the “Industry Sector” of a debtor (Nominal) must be weighed against their “Credit Rating” (Ordinal) to determine the discount rate for a funded invoice.

- Capital Markets: Where every microsecond of tick data (Time Series) from the Euronext or Deutsche Börse must be parsed for “Impossible Travel” or market manipulation patterns.

- Regulatory Compliance (KYC/AML): Where unstructured text in payment memos (Text), the pixel-level security features of a scanned Passport (Image), and even the vocal frequency of a customer during a verification call (Audio) converge to form a 360-degree risk profile.

Understanding data types is the prerequisite for effective Exploratory Data Analysis (EDA). Whether you are handling global SWIFT messages or satellite imagery for economic forecasting, your architectural decisions are governed by the underlying structure of your information. This guide provides a deep dive into the eight essential data types, focusing on the Data Scientist’s Point of View: why we choose specific encodings, where we apply them in production, and how we implement them in Python using pandas, numpy, and sklearn.

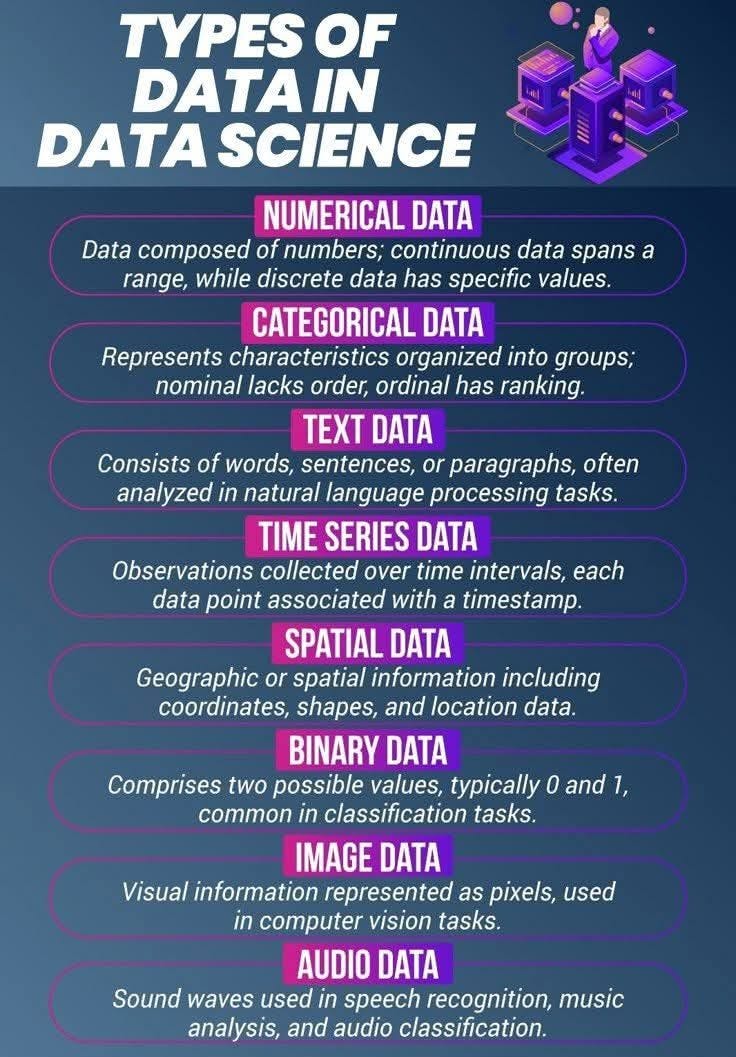

1. Numerical Data: The Signal of Magnitude

Numerical data represents quantitative measurements and is the bedrock of financial modeling. From a data scientist’s perspective, this is “low-entropy” data — it is highly structured and carries a high ratio of signal to noise. However, the way we handle these numbers depends entirely on whether they are Continuous or Discrete.

The Data Scientist’s POV: Why and Where?

As a professional, your first question when seeing numerical data is: “What is the distribution?”

Continuous Data (The Spectrum): These are measurements that can take any value within a range. In Stock Exchange Data, this is the fluctuating price of a ticker like SAP or ASML.

- Why handle it carefully? Most algorithms (like Neural Networks or Support Vector Machines) calculate distances. If one feature is “Annual Income in EUR” (range: 0–1M) and another is “Age” (range: 0–100), the model will be biased toward income purely because the numbers are larger.

- The DS Strategy: We use Standardization or Normalization to bring all continuous signals into a comparable range (usually 0 to 1 or a mean of 0).

Discrete Data (The Count): These are countable values that cannot be subdivided. In European Payments, this might be the number of SEPA (Single Euro Payments Area) transactions processed by a clearing house per hour.

- Why handle it carefully? While discrete data is numerical, it often acts like a category if the range is small (e.g., number of bank accounts: 1, 2, or 3). If the range is large (e.g., thousands of transactions), we treat it as continuous but watch for “spikes” or outliers.

- The DS Strategy: We look for “zero-inflation” — a common problem in banking where most customers have 0 defaults, but a few have many.

This code demonstrates how to handle these types for a machine learning pipeline, specifically focusing on scaling — the most critical step for any gradient-based learner.

import pandas as pd

import numpy as np

from sklearn.preprocessing import StandardScaler

# Scenario: European Stock Exchange (Euronext) monitoring

# We are tracking transaction counts (Discrete) and closing prices (Continuous)

data = {

'sepa_txn_count': [1200, 1550, 980, 2100, 1850], # Discrete: Countable transactions

'euronext_price': [145.20, 145.25, 145.18, 145.30, 145.28] # Continuous: Floating prices

}

df = pd.DataFrame(data)

# DATA SCIENTIST POV:

# Continuous variables require scaling to prevent "Gradient Explosion"

# or biased distance calculations in the model.

scaler = StandardScaler()

# We apply the scaler to the continuous price data

df['scaled_price'] = scaler.fit_transform(df[['euronext_price']])

# Result: 'scaled_price' now has a mean of ~0 and standard deviation of 1

print("Numerical Data - Production Ready Features:")

print(df)

2. Categorical Data: Nominal and Ordinal

Categorical data represents qualitative variables that describe groups or labels. From a Data Scientist’s perspective, these are not just labels; they are constraints on the geometry of your feature space. The way we encode these determines whether the model perceives a mathematical relationship between groups or treats them as entirely independent entities.

The Data Scientist’s POV: Why and Where?

When a Data Scientist encounters categorical data, the immediate priority is to identify the existence of a hierarchy.

Nominal Data (The Unordered Set): These are categories with no inherent ranking. In Invoice Finance, this could be the industry sector of the debtor (e.g., Retail, Manufacturing, Technology).

- The DS Strategy: We use One-Hot Encoding. Since “Retail” is not “greater than” “Tech,” we represent them as separate binary dimensions. However, we must be wary of the “Curse of Dimensionality” if there are hundreds of sectors. In production, we often group rare categories into an “Other” bucket to maintain model stability.

Ordinal Data (The Ranked Set): These are categories with a clear, logical order. In Risk Management, this is the internal credit rating assigned to a corporate borrower (e.g., AAA, AA, A, B).

- The DS Strategy: We use Label Encoding or Manual Mapping. From our POV, the “distance” between AAA and AA is a valuable signal. If we treat these as nominal, the model loses the understanding that AAA is safer than B. We manually map these to integers (4, 3, 2, 1) to preserve the directional trend of risk.

In this scenario, we process a portfolio of financed invoices. Notice how we handle the sector differently from the risk rating to ensure the model respects the underlying financial logic.

import pandas as pd

from sklearn.preprocessing import OneHotEncoder

# Scenario: Invoice Factoring Portfolio

# Industry (Nominal) vs. Internal Credit Grade (Ordinal)

data = {

'invoice_id': [101, 102, 103, 104],

'industry': ['Retail', 'Manufacturing', 'Tech', 'Retail'], # Nominal

'credit_grade': ['AAA', 'B', 'AA', 'A'] # Ordinal

}

df = pd.DataFrame(data)

# DATA SCIENTIST POV:

# 1. Manual Mapping for Ordinal data to preserve the "Risk Ladder"

risk_map = {'AAA': 4, 'AA': 3, 'A': 2, 'B': 1}

df['risk_score'] = df['credit_grade'].map(risk_map)

# 2. One-Hot Encoding for Nominal data

# We use drop_first=True to avoid the "Dummy Variable Trap" (Multicollinearity)

df_final = pd.get_dummies(df, columns=['industry'], drop_first=True)

print("Categorical Data - Preserving Financial Logic:")

print(df_final[['invoice_id', 'risk_score', 'industry_Manufacturing', 'industry_Tech']])

3. Text Data: Unstructured Semantic Signals

Text data consists of unstructured strings, such as words, sentences, or paragraphs. From a Data Scientist’s perspective, text is a high-dimensional sparse signal. Unlike numbers, computers cannot “read” text; we must transform it into a mathematical coordinate system — a process known as Vectorization or Embedding.

The Data Scientist’s POV: Why and Where?

In banking, text data is often the “smoking gun” in Anti-Money Laundering (AML) and Fraud Detection. We focus on extracting “semantic intent” from noisy strings.

Remittance Information (The “Why”): When a SEPA transfer is made, the “Purpose of Payment” field is often the only clue to the nature of the transaction. A Data Scientist looks for suspicious keywords or patterns that deviate from a user’s historical behavior.

The DS Strategy (TF-IDF vs. Embeddings): * For short, keyword-heavy text (like payment memos), we often use TF-IDF (Term Frequency-Inverse Document Frequency). This identifies which words are unique to a specific transaction relative to millions of others.

- For complex text (like legal contracts or chat logs), we use Word Embeddings (Word2Vec or Transformers) to capture context, recognizing that “Transfer funds” and “Send money” mean the same thing mathematically.

Where to use it: Categorizing expenses for personal finance apps, identifying sanctioned entities in cross-border transfers, and sentiment analysis of financial news for algorithmic trading.

Here, we simulate a pipeline that processes payment memos. We use TF-IDF because, in a production banking environment, identifying rare “trigger words” is more critical than complex sentence structure.

import pandas as pd

from sklearn.feature_extraction.text import TfidfVectorizer

# Scenario: AML Screening for European Cross-Border Payments

# Analyzing the "Remittance Info" field for suspicious patterns

memos = [

"Invoice payment for medical supplies REF-990",

"Internal transfer to savings account",

"Urgent payment for legal services",

"Payment for medical consultation"

]

# DATA SCIENTIST POV:

# We use TF-IDF to penalize common words like 'payment' or 'for'

# and highlight informative words like 'medical', 'legal', or 'savings'.

vectorizer = TfidfVectorizer(stop_words='english')

tfidf_matrix = vectorizer.fit_transform(memos)

# Converting to a DataFrame to visualize the high-dimensional feature space

text_features = pd.DataFrame(

tfidf_matrix.toarray(),

columns=vectorizer.get_feature_names_out()

)

print("Text Data - Semantic Feature Matrix:")

print(text_features)

4. Time Series Data: Sequential Dependency

Time series data is a sequence of observations collected at specific, often uniform, time intervals. From a Data Scientist’s perspective, this is the most “dangerous” data type because it violates the i.i.d. assumption (Independent and Identically Distributed). In most ML tasks, we assume row 1 has no impact on row 2; in Time Series, the fact that row 2 comes after row 1 is the most important feature you have.

The Data Scientist’s POV: Why and Where?

In High-Frequency Trading (HFT) and Liquidity Management, we don’t just look at the value; we look at the momentum and seasonality.

Temporal Dependency (The “Lag”): A Data Scientist knows that the price of a stock at 10:01 AM is highly correlated with its price at 10:00 AM.

- The DS Strategy: We use Lag Features. We shift the data to create new columns representing “Previous Price” or “Moving Average.” This allows standard algorithms to “see” the passage of time.

Stationarity: Financial data is often “non-stationary” (the mean and variance change over time).

- The DS Strategy: We rarely use raw prices. Instead, we calculate Log Returns or Differencing. This stabilizes the signal, making it easier for models to converge.

Where to use it: Predicting cash-out rates at ATMs across Europe, forecasting exchange rate volatility, and detecting anomalies in server logs for banking infrastructure.

This implementation shows how we transform raw tick data into a format suitable for a predictive model by engineering temporal relationships.

import pandas as pd

import numpy as np

# Scenario: High-Frequency Trading (HFT) Price Feed

# 1-minute interval bid prices for a specific ticker

time_index = pd.date_range(start='2026-01-16 09:00', periods=5, freq='min')

stock_data = pd.DataFrame({

'bid_price': [10.5, 10.6, 10.55, 10.7, 10.65]

}, index=time_index)

# DATA SCIENTIST POV:

# We cannot feed raw prices into a model and expect it to understand time.

# We must engineer 'Temporal Context'.

# 1. Create a Lag Feature (The price 1 minute ago)

stock_data['price_t_minus_1'] = stock_data['bid_price'].shift(1)

# 2. Calculate Percentage Change (Returns) to achieve stationarity

stock_data['returns'] = stock_data['bid_price'].pct_change()

# 3. Rolling Window (Moving Average) to smooth out noise

stock_data['rolling_mean_3min'] = stock_data['bid_price'].rolling(window=3).mean()

print("Time Series - Engineered Temporal Features:")

print(stock_data)

5. Spatial Data: Geographic Intelligence

Spatial data identifies the geographic location of features and boundaries on Earth, typically represented by coordinates (Latitude and Longitude). From a Data Scientist’s perspective, spatial data is about topological relationships — how close two events are in physical space and what that proximity implies about human behavior.

The Data Scientist’s POV: Why and Where?

In Retail Banking and Cybersecurity, geographic data is one of our most potent features for verifying the legitimacy of a digital event.

Distance and Velocity (The “Impossible Travel” Rule): A Data Scientist doesn’t just look at a login location; they look at the distance from the previous login.

- The DS Strategy: If a card is used in London at 10:00 AM and then in Paris at 10:15 AM, the calculated “velocity” is physically impossible. We use geometry to trigger immediate fraud alerts.

Clustering and Optimization: Banks use spatial data to decide where to place ATMs or branches.

- The DS Strategy: We use Point-of-Interest (POI) density. We analyze where customers spend money (e.g., high-end shopping districts vs. residential areas) to optimize physical infrastructure.

Geofencing: Setting virtual boundaries around sensitive locations (like a bank’s headquarters) to monitor unauthorized access attempts via mobile pings.

In this code, we calculate the proximity between a customer’s registered home address and their current transaction location. While complex apps use the Haversine formula (for the Earth’s curve), we often start with Euclidean distance for high-speed anomaly filtering.

import pandas as pd

import numpy as np

# Scenario: Fraud Detection - Distance between Home and Transaction

# Coordinates for London (Home) and Paris (Current Transaction)

spatial_data = pd.DataFrame({

'location_type': ['Home', 'POS_Transaction'],

'lat': [51.5074, 48.8566],

'lon': [-0.1278, 2.3522]

})

# DATA SCIENTIST POV:

# We need to calculate the "Spatial Delta".

# High delta in a short time-frame = High Probability of Fraud.

def calculate_simple_dist(coord1, coord2):

# Basic Euclidean distance for fast filtering in VS Code

return np.sqrt(np.sum((coord1 - coord2) ** 2))

home_coords = spatial_data.iloc[0, 1:3].values

txn_coords = spatial_data.iloc[1, 1:3].values

distance_delta = calculate_simple_dist(home_coords, txn_coords)

print(f"Spatial Data - Distance Delta: {distance_delta:.4f} degrees")

if distance_delta > 2.0:

print("Action: Flag for manual review - Potential Travel Anomaly.")

6. Binary Data: The Logic of Risk

Binary data is a specific case of categorical data that contains only two mutually exclusive states: 0 and 1, True and False, or Pass and Fail. From a Data Scientist’s perspective, binary data represents the Bernoulli Distribution. It is the most common format for a “Target Variable” — the thing we are actually trying to predict.

The Data Scientist’s POV: Why and Where?

In banking, almost every major decision boils down to a binary outcome. However, the challenge for a professional is almost always Class Imbalance.

The Rarity of Events (The Default Problem): In a healthy loan portfolio, 98% of people pay back their loans (Class 0) and only 2% default (Class 1).

- The DS Strategy: If you build a model that simply predicts “No Default” for everyone, you are 98% accurate, but you are a total failure as a Data Scientist because you caught zero risk. We don’t use Accuracy; we use Precision, Recall, and F1-Score to ensure we are catching the rare “1”s.

Probability Mapping: We rarely output a hard 0 or 1. Instead, we output a probability (e.g., 0.85).

- The DS Strategy: This allows the business to set a “Threshold.” For a small loan, we might approve anyone with a risk probability under 0.2. For a multi-million Euro corporate loan, that threshold might drop to 0.05.

Where to use it: Credit card approval (Approve/Reject), Fraud detection (Legit/Fraud), and Marketing (Click/No-Click).

This implementation focuses on analyzing the “Class Balance,” which is the very first step a professional takes before training a binary classifier.

import pandas as pd

# Scenario: Credit Approval System

# 1 = Approved, 0 = Rejected

binary_data = pd.DataFrame({

'loan_application_id': [5001, 5002, 5003, 5004, 5005],

'is_approved': [1, 0, 1, 1, 0]

})

# DATA SCIENTIST POV:

# Before modeling, we must calculate the "Event Rate".

# This determines if we need to use oversampling (SMOTE) or

# undersampling techniques to handle imbalanced classes.

approval_rate = binary_data['is_approved'].mean()

rejection_rate = 1 - approval_rate

print(f"Binary Data - Event Distribution:")

print(f"Approval Rate: {approval_rate * 100:.2f}%")

print(f"Rejection Rate: {rejection_rate * 100:.2f}%")

# Checking for imbalance

if approval_rate < 0.1 or approval_rate > 0.9:

print("Warning: Highly imbalanced dataset detected. Use specialized loss functions.")

7. Image Data: Visual Tensors

Image data is visual information represented as a grid of pixels. From a Data Scientist’s perspective, an image is not a picture; it is a 3D Tensor — a multi-dimensional array of numerical values representing the intensity of color (Red, Green, and Blue) across a spatial grid $(Height, Width, Channels)$.

The Data Scientist’s POV: Why and Where?

In modern banking, image data has moved from the back office to the front line through Digital KYC (Know Your Customer) and automated document processing.

Pattern Recognition vs. Pixels: A Data Scientist doesn’t look for a “face”; they look for “features.”

- The DS Strategy: We use Convolutional Neural Networks (CNNs). These models act as filters that slide across the pixel grid to detect edges, then shapes, and finally complex objects like a hologram on a passport or the biometric features of a face.

Security & Verification: * The DS Strategy (Liveness Detection): To prevent fraud, we analyze “Image Quality” and “Depth.” We use pixel-level analysis to determine if the camera is looking at a real person or a high-resolution photo being held up to a lens.

Where to use it: Verifying ID cards during mobile account opening, automated signature matching for cheques, and analyzing satellite imagery of retail parking lots to predict quarterly economic growth.

In this scenario, we simulate the processing of a small grayscale scan (like a barcode or signature fragment). We focus on Normalization, which is the single most important step for training visual models.

import numpy as np

# Scenario: Digital KYC - Processing a 5x5 grayscale scan of a signature fragment

# Values range from 0 (Black) to 255 (White)

image_pixels = np.array([

[10, 50, 255, 50, 10],

[50, 255, 100, 255, 50],

[255, 100, 20, 100, 255],

[50, 255, 100, 255, 50],

[10, 50, 255, 50, 10]

], dtype=np.uint8)

# DATA SCIENTIST POV:

# Raw pixel values (0-255) cause issues with Neural Network stability.

# We must 'Normalize' the tensor to a [0, 1] range.

normalized_image = image_pixels / 255.0

# For traditional ML models (like SVMs), we 'Flatten' the grid into a single vector.

flattened_vector = normalized_image.flatten()

print(f"Image Data - Original Shape: {image_pixels.shape}")

print(f"Image Data - Flattened Feature Vector (first 5 values):\n{flattened_vector[:5]}")

8. Audio Data: Frequency Domain Signals

Audio data represents sound waves captured over time. From a Data Scientist’s perspective, raw audio is a one-dimensional time-series signal measuring air pressure (amplitude). However, analyzing raw amplitude is rarely effective. Instead, we treat audio as a combination of different frequencies.

The Data Scientist’s POV: Why and Where?

In the banking sector, audio data is the primary frontier for Voice Biometrics and Customer Sentiment Analytics.

From Waveforms to Spectrograms (The “Visual” Sound): A Data Scientist knows that raw sound waves are messy.

- The DS Strategy: We use a Fourier Transform to convert audio from the “Time Domain” (amplitude over time) to the “Frequency Domain” (pitch over time). This creates a Spectrogram — essentially a heat map of sound frequencies. This allows us to use Image Classification techniques (like CNNs) to identify a person’s unique “voiceprint.”

Feature Extraction (MFCCs): Humans don’t hear all frequencies linearly; we are better at distinguishing lower pitches.

- The DS Strategy: We extract Mel-Frequency Cepstral Coefficients (MFCCs). These are features that represent the short-term power spectrum of a sound, specifically designed to mimic how the human ear perceives speech.

Where to use it: Voice-activated phone banking to prevent identity theft, detecting “frustration markers” in customer service calls to trigger manager intervention, and speech-to-text for logging financial advice for regulatory compliance.

This code simulates the generation of a sound wave (like a verification tone) and demonstrates how a professional calculates the “Energy” of the signal — a key feature used to detect the start and end of a person speaking.

import numpy as np

# Scenario: Voice Biometrics - Detecting a 440Hz verification tone

# 1 second of audio at a standard 16kHz sampling rate

sample_rate = 16000

duration = 1.0 # seconds

t = np.linspace(0, duration, sample_rate, endpoint=False)

# Generating a sine wave (A4 note)

audio_signal = np.sin(2 * np.pi * 440 * t)

# DATA SCIENTIST POV:

# Raw amplitude fluctuates between -1 and 1.

# To calculate the "strength" of the signal, we use Root Mean Square (RMS) energy.

# This helps distinguish between meaningful speech and background static.

rms_energy = np.sqrt(np.mean(audio_signal**2))

print(f"Audio Data - Total Samples: {len(audio_signal)}")

print(f"Signal Strength (RMS Energy): {rms_energy:.4f}")

# Pro-Tip: In production, we'd slice this into 'frames'

# to see how the energy changes every 20ms.

The Data Science Decision Matrix

As a professional, you need a mental framework to decide how to handle data the moment it hits your pipeline. The following matrix summarizes the strategic choices we make for each data type within a banking context.

To implement these concepts in a production environment, these are the industry-standard Python libraries I recommend for each data taxonomy:

- Numerical & Categorical: scikit-learn for preprocessing pipelines and pandas for high-performance data manipulation.

- Text Data: NLTK or spaCy for industrial-strength NLP, and Gensim for topic modeling.

- Time Series: statsmodels for statistical tests (like Stationarity) and Prophet for automated forecasting.

- Spatial Data: GeoPy for distance calculations and GeoPandas for handling spatial data frames.

- Binary Data: imbalanced-learn (SMOTE) to handle class imbalance in fraud or default datasets.

- Image Data: OpenCV for computer vision preprocessing and PyTorch or TensorFlow for deep learning.

- Audio Data: Librosa for extracting MFCCs and analyzing sound frequencies.

If you are working in VS Code and need to architect your pipeline in under 60 seconds, use this expert checklist to avoid common pitfalls:

- Distribution Check: If Numerical, is it Gaussian? If you see a “long tail” or heavy outliers, use PowerTransformer or RobustScaler instead of a standard scaler.

- Hierarchy Check: If Categorical, does “Category A > Category B”? If a rank exists, map it manually to integers. If no rank exists, use pd.get_dummies with drop_first=True to avoid multicollinearity.

- Dependency Check: If Time Series, is today’s value related to yesterday’s? Use the .shift() method to create "Lag" features. This is the only way for non-temporal models to understand the passage of time.

- Balance Check: If Binary, is your target event rare (e.g., Fraud < 2%)? Accuracy is a lie in this scenario. Use Precision-Recall curves and consider SMOTE (Synthetic Minority Over-sampling Technique) to balance your training set.

- Efficiency Check: If handling Text, Image, or Audio, are the raw dimensions overwhelming your compute? Use Dimensionality Reduction (like PCA) or leverage Pre-trained Embeddings from models like BERT or ResNet to keep your production code efficient.

Conclusion: The Professional’s Edge

Mastering these eight fundamental data types is the definitive boundary between a standard “modeler” and a high-impact Data Scientist. In the competitive arenas of European fintech, high-frequency trading, and digital banking, the transition from raw data to production-ready insight requires more than just clean Python code — it demands a deep mathematical intuition for the signals you are handling.

As you architect your next pipeline in VS Code, remember that your model is only as intelligent as the features you provide it. Whether you are normalizing pixel tensors for KYC or engineering lag features for market volatility, your choices in encoding and scaling will determine your model’s robustness in the high-pressure environment of global finance. Accuracy on paper is a starting point; reliability in production is the goal.

If you found this guide helpful and are looking to deepen your expertise in the field, I invite you to join our growing community of innovators. By clapping for this article, you help these insights reach a broader audience of developers and data enthusiasts who are navigating the same technical challenges. If you want to stay ahead of the curve with expert-level tutorials on AI, Machine Learning, and the evolving world of Financial Tech, make sure to follow my page. Sharing this content with your friends and professional network not only supports my work but also fosters a space where we can all learn and grow together. Thanks !!!

The Taxonomy of Information: A Professional Guide to Data Types in Modern Data Science was originally published in Towards AI on Medium, where people are continuing the conversation by highlighting and responding to this story.