Why the “SaaSpocalypse” story is wrong — and what’s actually happening underneath.

We’re now on SaaSpocalypse 2.0, 3.0, 4.0 , depending on whose count you trust. Every cycle, the obituary gets written: AI will kill enterprise SaaS, Salesforce is dead, ServiceNow is dead, Workday is dead. One bad ServiceNow print this quarter sent the whole sector down 5–10% on a single day. P/E multiples on quality software names compressed to 10–12x. Investors hit sell first and asked questions later.

It’s a fun story. It’s also wrong.

Here’s what’s interesting: customers haven’t changed their software buying behavior. Not really. Procurement teams will tell you they’d love to save money, but no one is ripping out Salesforce or canceling Workday because of a chatbot demo. The selloff isn’t driven by collapsing fundamentals. It’s driven by something more specific, and more fixable.

What investors are actually pricing in is uncertainty about the business model, not the death of the software. Per-seat licensing is predictable; agent-driven, consumption-based revenue is nebulous. Predictable becomes nebulous, multiples compress. That’s it. That’s the whole panic.

But “the pricing model is changing” is a very different story from “SaaS is dead.” And once you separate those two stories, the real picture comes into focus. The SaaS stack isn’t collapsing. It’s being re-layered.

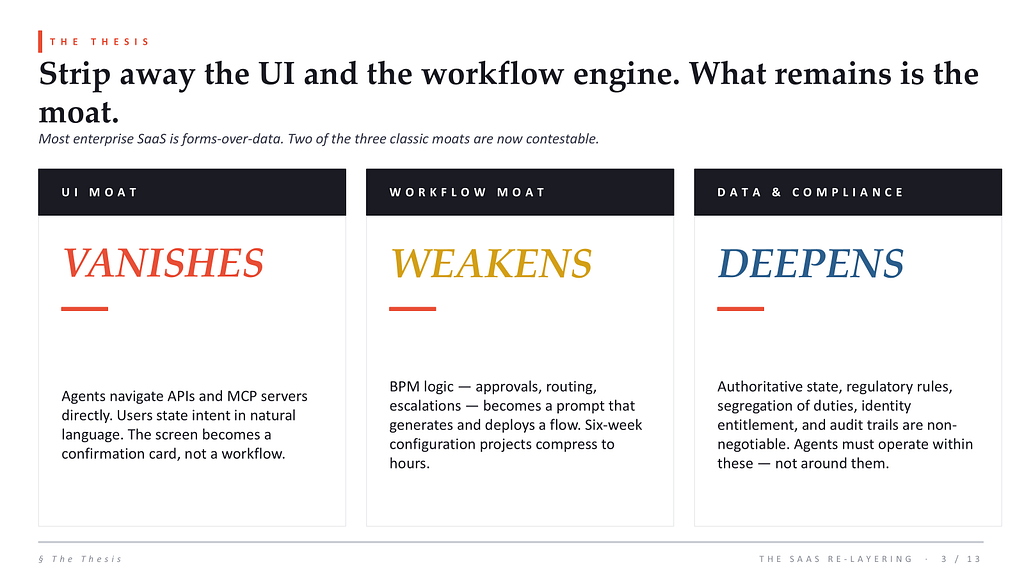

The thesis in one sentence

Most enterprise SaaS is forms-over-data with a workflow engine on top. Of the three classic moats — UI, workflow, and data/compliance — agents make two of them contestable. The third gets stronger.

The UI moat vanishes because users stop clicking through nine screens and start telling agents what they want. The workflow moat weakens because BPM logic that used to take a six-week configuration project becomes a prompt. But the data and compliance moat deepens, authoritative state, segregation of duties, audit trails, identity entitlement, regulated business rules. None of that goes away. Agents have to operate inside it, not around it.

So the giants don’t get replaced. Their middle thins out.

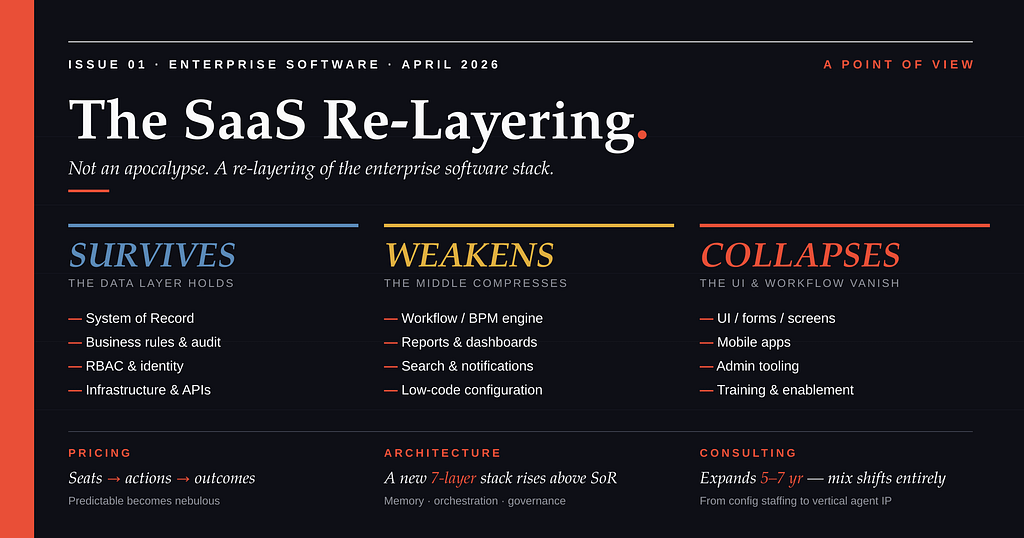

What survives, weakens, and collapses

Not every SaaS component fares the same way. Some get disrupted. Some take advantage. The trick is knowing which is which before you place a bet.

Strip enterprise SaaS down to its components and there are about fifteen of them — the System of Record, business rules, audit, RBAC, multi-tenancy, the API surface, the workflow engine, dashboards, search, notifications, low-code, the UI, mobile apps, admin tooling, training. Score each one for how it fares in an agent-led world and a clear pattern emerges.

The bottom of the stack, data, rules, identity, audit, integrations, survives or strengthens. The top of the stack, UI, mobile, admin tooling, training, largely collapses. The middle, workflow, dashboards, search, notifications, configuration, weakens, gets generated on demand, becomes a feature instead of a product.

If you’re trying to figure out where to build, the collapse and weaken bands are your opportunity zone.

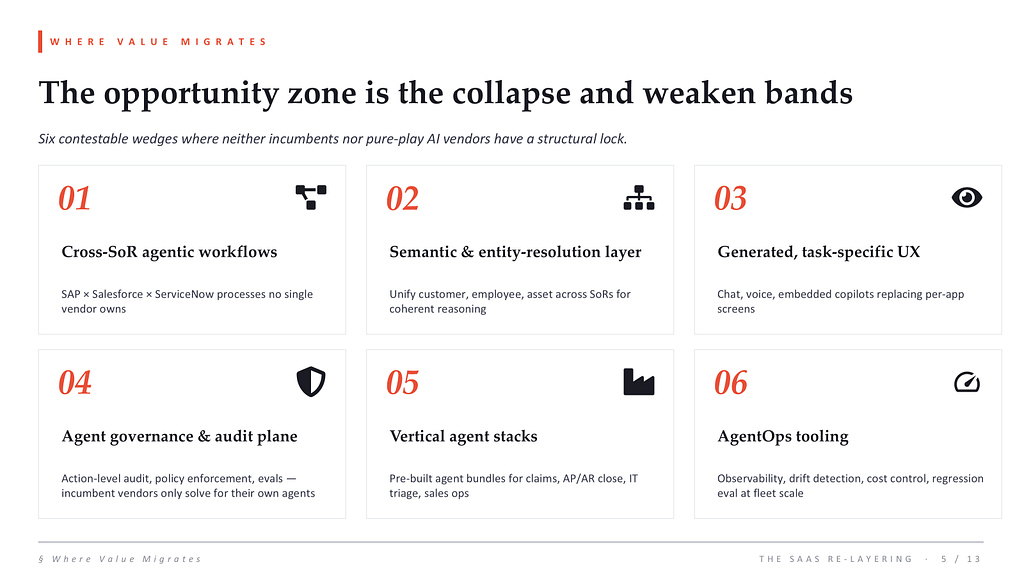

Where value migrates

Six wedges, none of which a single platform vendor can structurally own.

Cross-SoR workflows aren’t owned by SAP, Salesforce, or ServiceNow alone, they cross all of them. Entity resolution across systems is hard, and necessary, and not the SoR vendor’s natural job. Governance and AgentOps are universal needs that incumbents only solve for their own agents. Vertical agent stacks, claims, AP/AR, IT triage , pre-bundle deep industry IP. Generated UX replaces per-app screens.

These are the contested middle. This is where new companies get built.

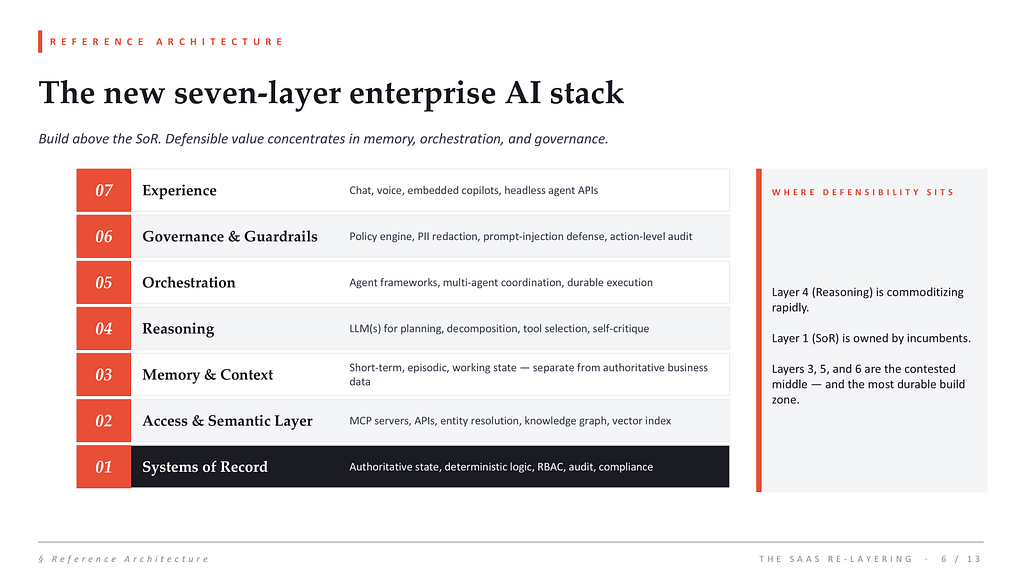

The new seven-layer stack

Above the System of Record, a new architecture is taking shape. Seven layers. The defensible value sits in the middle ones — not the model, not the database.

The reasoning layer, the LLM itself, is commoditizing fast. Frontier models trade places every few months. The data layer is owned by incumbents who are racing to embed their own agents.

The durable build zone is memory, orchestration, and governance. Memory because authoritative business data lives in the SoR, but agent context doesn’t. Orchestration because multi-agent coordination, durable execution, and tool-use planning are non-trivial. Governance because regulated industries cannot deploy agentic systems without action-level audit, delegated identity, and policy enforcement.

What agents actually do

Use cases ranked roughly by enterprise willingness-to-pay, which is also a rough proxy for how close the work sits to revenue, compliance, or recurring labor cost.

Replacing data entry alone justifies most of the spend. Tier-1 ticket triage is the biggest cost-takeout opportunity in IT and customer service. Cross-system orchestration , quote-to-cash, hire-to-retire, procure-to-pay, is where the real money lives, because it’s where the SoR vendors structurally can’t serve customers well. Continuous close, compliance copilots, and outcome-aligned outreach come next. The mobile UX collapse, voice-driven field operations for technicians and nurses, is the dark horse.

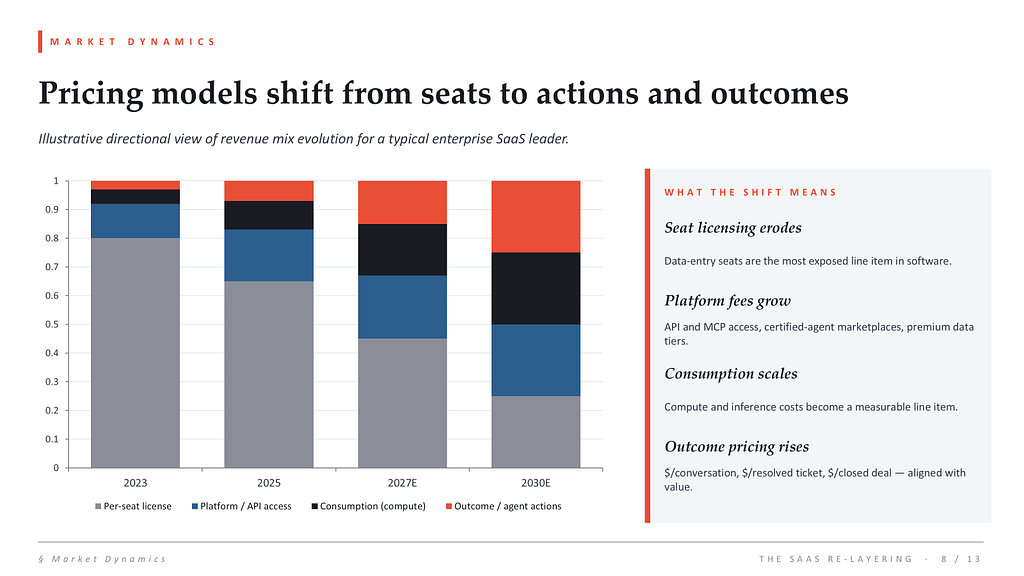

Pricing breaks first

The seat license is the first business model to die. It assumes a human sitting at a screen, doing work that an agent now does. The replacement is a hybrid , a thinner platform fee plus consumption plus outcome-aligned charges.

This is the real reason the market panicked. Not because SaaS is dead , but because what was predictable (seats × ARPU × retention) becomes nebulous (tokens, actions, outcomes, with usage that varies wildly by customer and quarter). Harder to model means lower multiples, even when the underlying business is fine. Vendors who lead this transition control the narrative. Vendors who get dragged through it lose twice; once in the shift, once in the messy quarter when investors realize what’s happening.

Per-seat goes from ~80% of revenue to under 25% over the next five-to-seven years. Platform and API fees grow. Consumption (compute, inference) becomes a real line item. Outcome pricing , $/conversation, $/resolved ticket, $/closed deal, rises fastest in percentage terms, even if it’s still a minority of total revenue by 2030.

If you’re a vendor, you want to lead this transition, not get dragged through it.

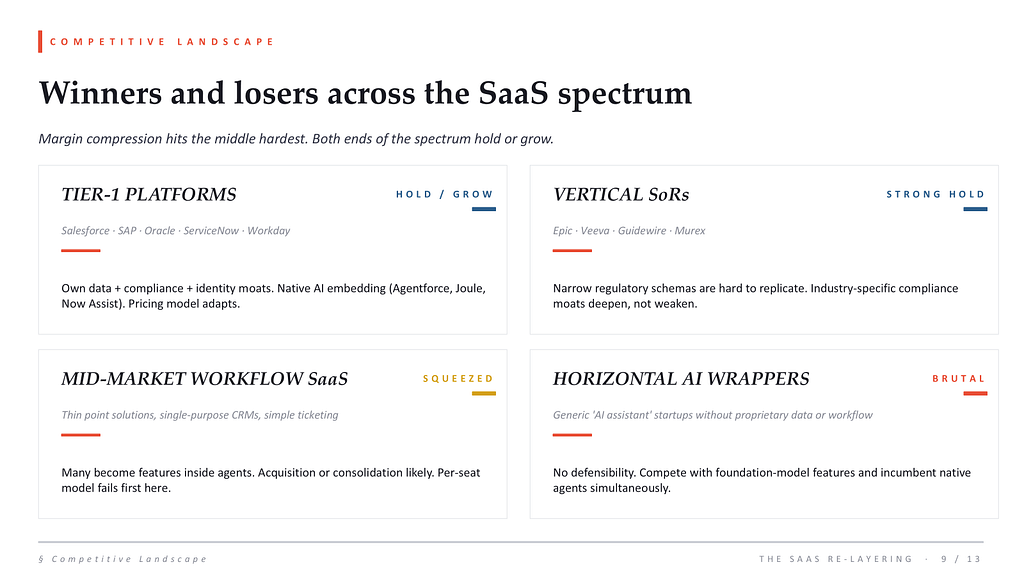

Winners and losers

Margin compression hits the middle hardest. Both ends of the spectrum hold or grow.

Tier-1 platforms (Salesforce, SAP, Oracle, ServiceNow, Workday) hold their moats, and they’re embedding AI natively. Vertical SoRs (Epic in healthcare, Veeva in life sciences, Guidewire in insurance) hold even stronger because regulated schemas are hard to replicate. Mid-market workflow SaaS, thin point solutions, single-purpose tools, gets squeezed; many become features inside agents. Horizontal AI wrappers without proprietary data or workflow have the worst position: they compete with foundation-model native features and incumbent agents simultaneously.

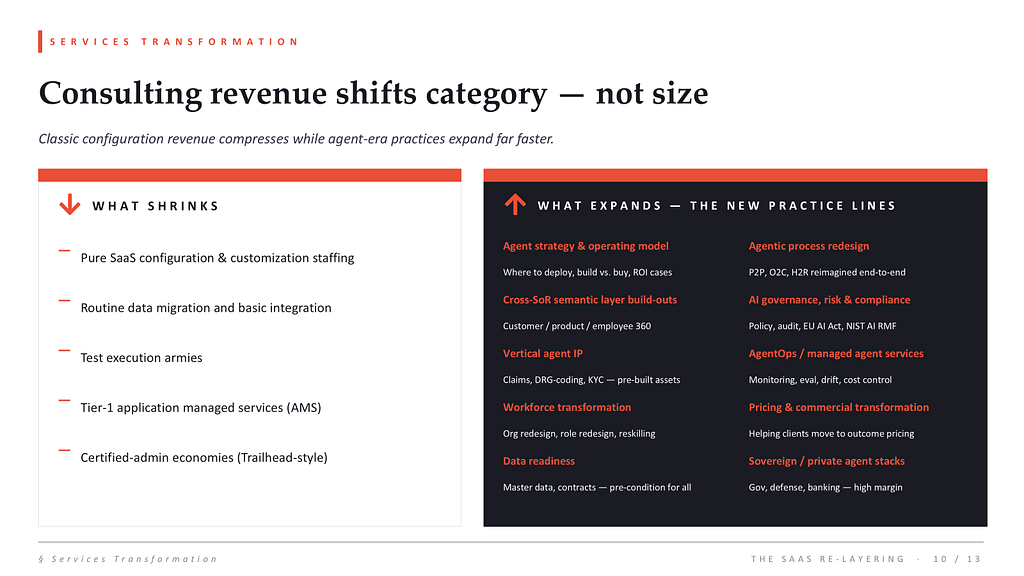

Consulting transforms and grows

Conventional wisdom says generative AI kills systems-integrator revenue because configuration becomes self-serve. The opposite happens, at least for the next five-to-seven years.

What shrinks: SaaS configuration staffing, routine integration build-out, test execution armies, basic application managed services. What expands: agent strategy, agentic process redesign, semantic-layer build-outs, AI governance, vertical agent IP, AgentOps, workforce transformation, pricing transformation, data readiness, sovereign agent stacks. The mix shifts entirely. The big firms that move fastest into agent-era practices end up with bigger books — at higher margins.

The numbers that matter

A directional view: about 70% of paid SaaS UI surface area gets displaced or wrapped by agents. A 5–7 year window of net consulting demand growth as the mix transforms. A 3–5x premium for outcome-priced agent services over seat licenses. Tier-1 SaaS revenue from seats drops below 25% by 2030. Six contestable wedges where incumbents lack a structural lock. Seven layers in the new stack above the SoR.

Estimates are illustrative — synthesized from public vendor disclosures, analyst commentary, and a point of view. Actuals will vary by industry and platform.

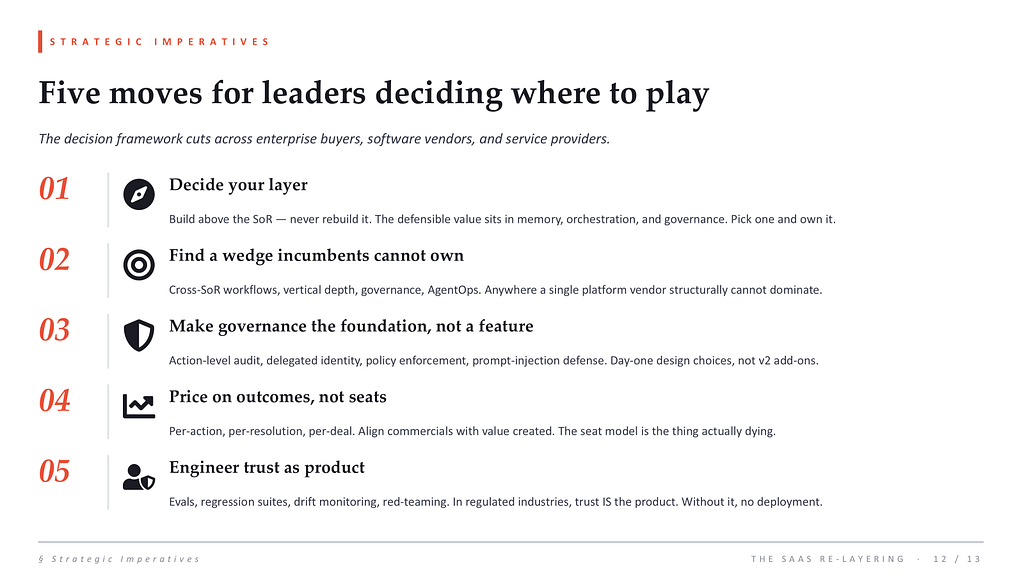

Five moves for leaders

Decide your layer. Build above the SoR, never rebuild it. Pick memory, orchestration, or governance and own it.

Find a wedge incumbents can’t own. Cross-SoR, vertical depth, governance, AgentOps. Anywhere a platform vendor structurally cannot dominate.

Make governance the foundation, not a feature. Action-level audit, delegated identity, policy enforcement, prompt-injection defense. Day-one design choices. In regulated industries, you don’t deploy without these.

Price on outcomes, not seats. Per-action, per-resolution, per-deal. Align commercials with value created. The seat model is the thing actually dying.

Engineer trust as product. Evals, regression suites, drift monitoring, red-teaming. In regulated industries, trust IS the product.

Closing

The middle of the SaaS stack is being rewritten. The data layer holds. The UI and workflow layers thin out. A new stack of memory, orchestration, and governance rises above. Pricing shifts from seats to actions. Consulting expands at the same time it transforms.

For enterprise buyers: re-baseline your SaaS spend against agent economics. The seat budget is the wrong starting point. For software vendors: move pricing toward consumption and outcomes before customers force the conversation. For service providers: productize vertical agent IP. The era of staffing-led SaaS implementation is closing.

It’s not an apocalypse. It’s a re-layering. And the question for everyone in the stack is the same one; which layer do you choose to own?

If this resonated, share it. If it didn’t, tell me why — that’s where the interesting conversations live.

Disclaimer

The views, analysis, and opinions expressed in this article are solely my own and are presented in my personal capacity. They do not represent the views, positions, opinions, or official statements of my employer, any clients, partners, vendors, or organizations I am affiliated with, now or in the past. This content is provided for informational and educational purposes only. Nothing here constitutes investment, legal, tax, or financial advice, nor should it be interpreted as a recommendation to buy, sell, or hold any security, asset, or instrument. Valuations, revenue figures, and projections are based on publicly reported information at the time of writing and may change. Readers should conduct their own due diligence and consult qualified professionals before acting on any of the ideas presented here.

SaaS Isn’t Dying. It’s Being Re-Layered was originally published in Towards AI on Medium, where people are continuing the conversation by highlighting and responding to this story.