On September 11, Oracle stock stood at about $308, following a giant leap based on reports of a deal with OpenAI. Euphoria was in the air; the stock was up for 43%.

But I wasn’t buying, and I wrote an essay here called Peak Bubble, which read it in part:

OpenAI doesn’t have $300 billion dollars

They don’t have anywhere near $300 billion dollars

By their own (presumably optimistic) projection, they won’t turn a profit until 2030.

And all this from a company thought (or claimed) that GPT-5 was going to be tantamount to AGI (spoiler alert: it wasn’t)

For good measure Oracle doesn’t have the chips they would need to fulfill the contracts, or even the cash to buy them.

I won’t say that it is all make-believe, but, well, you do the math…

If Oracle actually collects its $300 billion, I will truly be astounded.

Today, even after a very strong week, Oracle stands at just $170.

But my point then wasn’t that Oracle would never rise from that point (it actually did, briefly), but that in hindsight some years from now, people would think that that spike in Oracle’s stock was the peak of absurdity.

Maybe I spoke too soon.

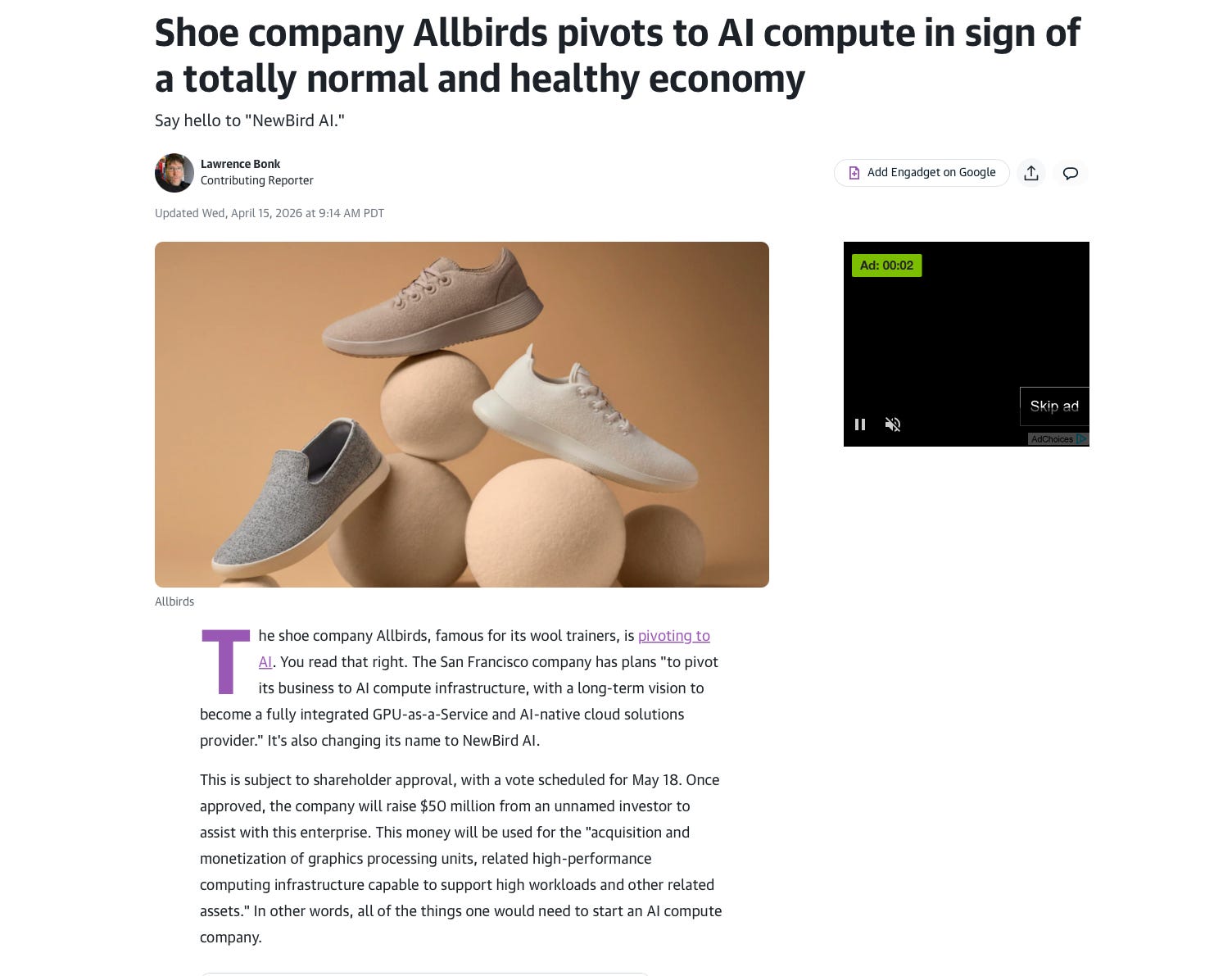

As of today, there’s a new kid in town:

I can’t top this summary of the above, and won’t try: