The Blind Speed of Adoption: How Financial Advisors Are Racing to Embrace AI — While Leaving Client Data Privacy in the Dust

Introduction: The Great AI Gold Rush in Financial Advisory

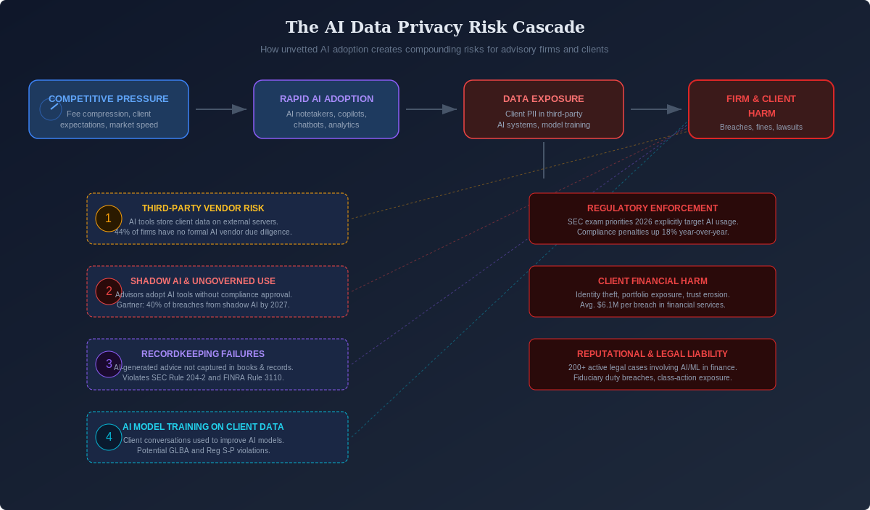

There is a gold rush underway in the $130 trillion global wealth management industry, and its currency is artificial intelligence. From the corner offices of wire houses on Wall Street to the home offices of independent registered investment advisors in suburban America, the message is the same: adopt AI or risk irrelevance. The pressure is real, measurable, and relentless. Fee compression is squeezing margins. Client expectations, shaped by the frictionless digital experiences of fintech disruptors, are rising. And the sheer volume of data that advisors must synthesize — market intelligence, tax optimization strategies, estate planning nuances, behavioral finance cues — has long surpassed what any single human mind can efficiently process.

So advisors are turning to artificial intelligence. They are deploying AI-powered meeting notetakers that transcribe and summarize every word of a client conversation. They are feeding sensitive portfolio data into generative AI copilots that promise to draft financial plans in minutes rather than hours. They are using AI chatbots trained on proprietary client information to answer internal queries, and they are subscribing to predictive analytics platforms that ingest deeply personal financial data to generate investment recommendations.

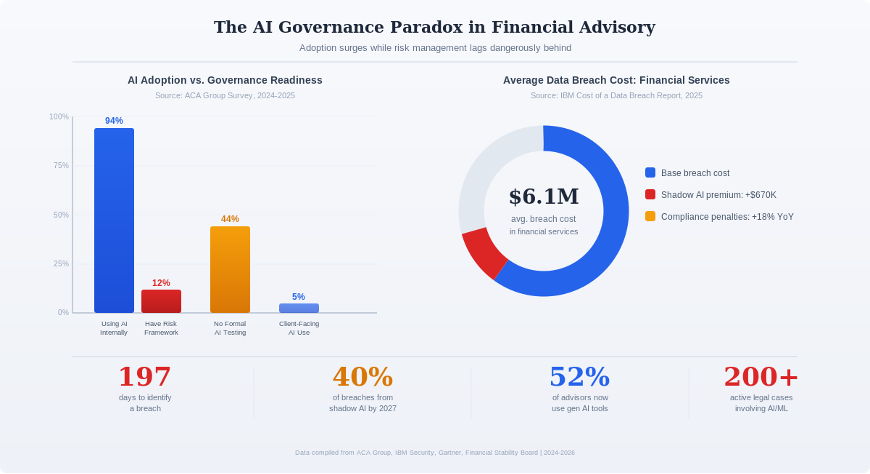

The adoption numbers tell a staggering story. As of early 2026, 52% of financial advisors now use one or more generative AI tools in their practice, up from 41% just a year earlier. Roughly 94% of financial services firms are piloting or deploying generative AI within core business functions. The technology is no longer experimental — it is operational, embedded, and expanding at a pace that should alarm anyone paying attention to what happens to client data along the way.

Because here is the uncomfortable truth that the industry’s breathless AI evangelism conveniently omits: the vast majority of these firms have given almost no serious thought to the data privacy implications of what they are doing. They are plugging client Social Security numbers, net worth figures, health information, family dynamics, and tax records into third-party AI systems with little understanding of where that data goes, how it is stored, who can access it, or whether it is being used to train the very models that serve their competitors.

Jump.ai, “AI Tools for Financial Advisors,” April 2026. Reports 52% of financial advisors now use generative AI tools, up from 41% in 2025.

“Only 12% of financial services firms using AI have any formal risk management framework in place. The other 88% are flying blind with their clients’ most sensitive data.”

The Pressure Cooker: Why Advisors Are Adopting AI Without Looking

To understand why financial advisors are making these decisions, you have to understand the existential pressure they face. The wealth management industry is heading into 2026 with solid markets but a business model under siege.

Oliver Wyman’s 2026 wealth management outlook describes it bluntly: years of rate tailwinds offered temporary relief on cost pressure, masking structural complexities within many established cost bases. Many wealth managers are hampered by burdensome manual processes, a reliance on legacy systems, and operating models that are simply not fit for purpose in a world where clients expect instant, personalized, data-rich advice.

The competitive dynamics are fierce. Robo-advisors have driven fee expectations downward. Younger, digitally native clients view AI-augmented advice not as a luxury but as a baseline expectation. Meanwhile, the largest firms — the Morgan Stanleys, the JPMorgans, the Schwabs — are investing hundreds of millions in proprietary AI platforms, creating a capability gap that independent advisors and smaller RIAs fear they cannot bridge.

AI promises to be the great equalizer. A solo practitioner with the right AI stack can now generate financial plans, draft client communications, research investment opportunities, and manage compliance documentation at a speed and quality that previously required a team of analysts. The temptation is irresistible: deploy AI tools today, figure out the compliance and privacy implications later.

This “move fast and figure it out later” mentality is precisely where the danger lies. In the rush to stay competitive, advisors are treating AI adoption as a technology decision when it is fundamentally a data governance decision — one with regulatory, legal, ethical, and fiduciary implications that most firms have barely begun to contemplate.

The Tools They’re Adopting — And What Those Tools Consume

Consider the AI tools now commonplace in advisory practices. AI-powered meeting notetakers — products like Otter.ai, Fireflies, and specialized financial services tools like Zocks and Jump — sit silently in client meetings, capturing every word. They record discussions about a client’s cancer diagnosis and its estate planning implications. They capture conversations about a messy divorce and the asset division strategy. They transcribe sensitive tax situations, business succession plans, and family conflicts over inheritance.

All of this data — the most intimate details of a person’s financial life — is then processed on third-party servers, often stored in cloud environments the advisor has never audited, and in many cases used to improve the AI models themselves. As the Financial Planning Association’s journal recently noted, “AI tools may potentially expose sensitive information to privacy risks” that most practitioners have not adequately assessed.

Portfolio AI copilots take this further. Advisors feed entire client portfolios — holdings, performance history, risk tolerance assessments, stated goals — into generative AI systems to receive optimization suggestions. Predictive analytics platforms ingest years of client transaction data to model future behavior. Each of these tools creates a new vector through which client data can be exposed, misused, or compromised.

Figure 1: The Regulatory Gap — Client data falls through the widening chasm between existing regulation and the pace of AI innovation.

The Regulatory Landscape: Robust on Paper, Fragile in Practice

Defenders of the current approach will point to the substantial body of regulation already governing data privacy in financial services. They are not wrong that significant regulatory infrastructure exists. The SEC, FINRA, and related agencies have established a framework that, on paper, should provide meaningful client protections. But the critical question is whether these regulations were designed for — or are capable of addressing — the specific data privacy challenges that AI introduces.

Regulation S-P: The Foundation with New Cracks

The SEC’s Regulation S-P, originally adopted under the Gramm-Leach-Bliley Act, is the primary federal rule governing the privacy of consumer financial information. In May 2024, the SEC issued significant amendments that took effect in December 2025 for larger firms (those with $1.5 billion or more in assets under management) and will take effect in June 2026 for smaller firms.

These amendments are substantive. They now require written incident-response programs designed to detect, respond to, and recover from unauthorized access to customer information. They mandate notification to affected individuals within 30 days of a breach, absent a “no-harm” finding. They expand the definition of “customer information” to include all client data in the firm’s possession or handled by third parties on the firm’s behalf — a provision with enormous implications for AI tool usage.

But here is where theory diverges from practice. Regulation S-P was conceived in a world where client data lived in filing cabinets, proprietary databases, and controlled internal systems. It was not designed for a world where an advisor’s AI notetaker sends a real-time transcript of a client meeting to a server farm operated by a startup in San Francisco, where the data may be used to fine-tune a large language model that serves thousands of other users.

FINRA’s 2026 Oversight Report: Sounding the Alarm

FINRA’s 2026 Annual Regulatory Oversight Report, published in December 2025, dedicated an entire section to generative AI — a first in its history. The nearly 90-page report explicitly identified several regulatory risks for member firms associated with AI use, including recordkeeping, customer information protection, risk management, and compliance with Regulation Best Interest (Reg BI).

FINRA’s guidance is clear: firms should ensure their supervision and governance practices cover AI use cases, model risks, fair and balanced customer communications, vendor diligence, capture of AI-enabled communications within firm books and records, and technology change management. Firms should conduct initial and ongoing due diligence of vendors supporting mission-critical systems, maintain detailed inventories of vendor services and the firm data they access, and ensure that contracts contain robust data-protection, confidentiality, and GenAI-related restrictions.

The language is measured but the implications are stark. FINRA is effectively telling the industry: we know you are adopting AI, we know you are not doing sufficient due diligence on how these tools handle client data, and we will be examining you on this.

SEC 2026 Examination Priorities: AI Under the Microscope

The SEC’s Division of Examinations has made its 2026 priorities equally explicit. The Division will evaluate whether firms’ actual AI usage matches their representations to clients and regulators. Firms claiming to use AI for portfolio management must demonstrate that AI tools genuinely influence investment decisions rather than serve merely as supplemental research. Reviews will assess cybersecurity governance, identity theft prevention controls, vendor oversight, and preparedness for sophisticated cyber threats, including AI-driven intrusions.

This is significant. The SEC is not merely asking whether firms have policies about AI — it is asking whether those policies are real, operational, and adequate. It is a signal that enforcement actions are coming for firms that adopt AI carelessly.

“The SEC is not merely asking whether firms have policies about AI — it is asking whether those policies are real, operational, and adequate. Enforcement actions are coming.”

Oliver Wyman, “10 Wealth Management Trends for 2026,” December 2025.

Financial Planning Association Journal, “The Compliance Risks of Using Generative AI in a Financial Planning Practice,” May 2025.

FINRA, “2026 Annual Regulatory Oversight Report,” December 2025.

SEC, “Amendments to Regulation S-P,” May 2024. Compliance required December 3, 2025 for large firms; June 3, 2026 for smaller entities.

Goodwin Law, “2026 SEC Exam Priorities for Registered Investment Advisers,” December 2025.

The Risks They’re Not Seeing

Despite the regulatory framework in place, the specific risks created by AI adoption in financial advisory are neither well understood nor adequately managed by most firms. These risks fall into several interconnected categories, each compounding the others.

Risk 1: Third-Party Vendor Data Exposure

When a financial advisor subscribes to an AI notetaker or a generative AI copilot, they are entering into a data-sharing arrangement with a third party. In many cases, these third parties are venture-backed startups with minimal track records in data security. The client’s Social Security number, discussed casually in a meeting about tax planning, is now sitting on a server the advisor has never inspected, governed by a terms-of-service agreement the advisor likely never read.

A 2024 survey found that 44% of firms have no formal testing or validation of the outputs from their AI tools, let alone auditing of how those tools handle input data. Before deploying any AI tool, firms must understand whether they can opt out of data training, or if the vendor provides a “walled garden” environment that protects client information. Most have not asked these questions.

Risk 2: Shadow AI and Ungoverned Adoption

Perhaps the most insidious risk is what the industry now calls “shadow AI.” This is the use of AI tools by employees without the knowledge or approval of compliance departments. A junior associate pastes a client’s tax return into ChatGPT to draft a summary. An advisor uploads a client portfolio to an AI platform they found on Product Hunt. A paraplanner uses a free AI meeting summarizer that stores data indefinitely. Gartner predicts that 40% of data breaches will be attributed to misuse of AI or shadow AI systems by 2027. Organizations with unmonitored shadow AI faced breach costs averaging $670,000 higher than those with stricter controls.

Risk 3: AI Model Training on Client Data

Many AI platforms use the data they receive to improve their models. This means that a client’s financial plan, discussed in a meeting captured by an AI notetaker, could theoretically inform the model’s responses to other users. While most enterprise AI vendors offer opt-out mechanisms, the default settings often allow data use for model improvement. Few advisors understand these settings, and fewer still have negotiated custom data-handling agreements with their AI vendors.

This creates a potential violation of the Gramm-Leach-Bliley Act, which restricts the sharing of nonpublic personal information. It also raises questions under Regulation S-P’s expanded definition of customer information protection. If a client’s financial data is used to train a model that then serves other clients — including potentially competitors’ clients — the advisor may be breaching their fiduciary duty without even knowing it.

Risk 4: Record keeping and Compliance Gaps

SEC Rule 204–2 and FINRA Rule 3110 require advisory firms to maintain books and records of their advice and communications. When an advisor uses an AI copilot to draft a financial plan recommendation, that AI-generated output is arguably a communication that must be captured, reviewed, and retained. Most firms have not updated their recordkeeping practices to account for AI-generated content.

Furthermore, when an AI tool provides a recommendation that an advisor then communicates to a client, questions arise about the firm’s obligation under Reg BI to ensure that recommendation is in the client’s best interest. If the AI model has inherent biases — trained on historical data that reflects past market conditions or demographic patterns — the advisor may unknowingly be delivering biased advice while believing they are using cutting-edge technology.

Risk 5: The Breach Cost Calculus

The financial consequences of getting this wrong are severe. According to IBM’s 2025 Cost of a Data Breach Report, the average breach cost in financial services is $6.1 million, with compliance-related penalties increasing 18% year-over-year. The average time to identify a breach is 197 days — more than six months during which client data may be exposed without anyone’s knowledge. And with over 200 active legal cases involving AI and machine learning in finance, the litigation landscape is expanding rapidly.

ACA Group, “Investment Adviser Compliance Survey,” 2024. Found that only 12% of financial services firms using AI have any formal risk management framework.

Gartner Research, 2025. Predicts 40% of data breaches will be attributed to misuse of AI or shadow AI systems by 2027.

IBM Security, “Cost of a Data Breach Report,” 2025. Financial services sector average breach cost: $6.1 million.

Financial Stability Board, “Monitoring Adoption of AI and Related Vulnerabilities in the Financial Sector,” October 2025.

The Fiduciary Paradox: When Efficiency Undermines Duty

Financial advisors operate under a fiduciary standard — a legal and ethical obligation to act in their clients’ best interests. This is the highest standard of care recognized in law. It is the reason clients trust their advisor with information they would not share with their closest friends: their true net worth, their health conditions, their family conflicts, their fears about the future.

The fiduciary paradox of AI adoption is this: advisors adopt AI tools to serve clients better — to be more efficient, more comprehensive, more responsive — but in doing so, they may be exposing those same clients to data privacy risks that fundamentally violate the trust relationship. The advisor who uses an AI copilot to generate a more thorough financial plan may be simultaneously feeding that client’s most sensitive data into a system with inadequate protections.

This is not a hypothetical concern. It is a structural tension at the heart of the current AI adoption wave. The tools that promise better outcomes for clients are the same tools that create new pathways for client harm. And the firms that adopt most aggressively — driven by competitive pressure — are often the ones with the least robust data governance frameworks.

“The tools that promise better outcomes for clients are the same tools that create new pathways for client harm. That is the fiduciary paradox of AI in financial advice.”

What Firms and Regulators Must Do Now

The situation is urgent but not hopeless. There are concrete steps that advisory firms, regulators, and the industry at large can take to close the gap between AI adoption and data privacy protection.

For Advisory Firms

First, establish an AI governance framework before deploying any new AI tool. This means creating a cross-functional committee that includes compliance, technology, legal, and advisory leadership. Every AI tool should undergo a formal data privacy impact assessment before deployment, examining where client data goes, how it is stored, whether it is used for model training, and what happens to it when the vendor relationship ends.

Second, conduct rigorous vendor due diligence. This goes beyond reading a vendor’s privacy policy. It means demanding SOC 2 Type II compliance, negotiating custom data processing agreements that explicitly prohibit the use of client data for model training, ensuring data residency requirements are met, and establishing contractual obligations for breach notification that exceed the 30-day window required by Regulation S-P.

Third, address shadow AI head-on. Implement technical controls that prevent unauthorized AI tool usage, but also create approved AI toolkits that give advisors the productivity gains they need within a governed framework. If you make it easy to use the right tools, employees are less likely to reach for ungoverned alternatives.

Fourth, update recordkeeping practices. Every AI-generated recommendation, every AI-summarized meeting, every AI-drafted communication should be captured in the firm’s books and records as required by SEC and FINRA rules. This is not optional — it is a regulatory obligation that most firms are currently failing to meet.

For Regulators

The SEC and FINRA have taken important first steps, but more is needed. The current regulatory approach — applying existing rules to novel AI use cases — is necessary but insufficient. Regulators should develop specific guidance on AI vendor due diligence requirements, establish minimum data privacy standards for AI tools used in financial advisory, and create a framework for evaluating whether AI-generated advice meets the best interest standard under Reg BI.

Colorado’s Senate Bill 24–205, which becomes effective in February 2026 and requires financial institutions to disclose how AI-driven decisions are made including the data sources involved, offers a model for federal action. The patchwork of state-level AI regulations currently emerging creates compliance complexity; a federal framework would provide needed clarity.

For the Industry

Industry organizations — the Financial Planning Association, the CFP Board, SIFMA, the Investment Adviser Association — should develop industry-wide standards for AI data privacy in financial advisory. This includes establishing certification programs for AI vendors serving the industry, creating shared frameworks for AI risk assessment, and building educational programs that help advisors understand the data privacy implications of the tools they use.

The Road Ahead: Navigating the AI-Privacy Tightrope

The financial advisory industry stands at an inflection point. AI will transform how advice is delivered — that much is certain. By 2027, the most competitive firms will not be asking whether to adopt AI, but how to apply it most effectively. The question is whether this transformation will happen in a way that protects or endangers the clients it purports to serve.

The data is clear. Adoption is outpacing governance by a wide margin. Ninety-four percent of firms are using AI, but only twelve percent have formal risk frameworks. Forty-four percent have no testing or validation processes for their AI tools. The regulatory apparatus, while strengthening, was built for a pre-AI world and is struggling to keep pace. And the financial consequences of failure — $6.1 million average breach costs, 18% annual increases in compliance penalties, a growing wave of AI-related litigation — are severe and escalating.

Clients trust their financial advisors with the most sensitive information in their lives. That trust is the foundation of the entire advisory relationship, and it is built on the implicit promise that the advisor will protect that information with the same care they would their own. When advisors feed that data into AI systems without adequate safeguards, they are not just creating regulatory risk — they are betraying a sacred trust.

The firms that will thrive in the AI era are not the ones that adopt fastest. They are the ones that adopt smartest — building robust data governance frameworks, demanding transparency from their AI vendors, updating their compliance infrastructure, and never losing sight of the fact that every data point they process represents a real person’s financial life.

The blind speed of adoption must give way to the clear sight of responsibility. The technology is ready. The question is whether the industry is.

The Blind Speed of Adoption: How Financial Advisors Are Racing to Embrace AI — While Leaving Client… was originally published in Towards AI on Medium, where people are continuing the conversation by highlighting and responding to this story.